DYNAMIC DOUBLE MATERIALITY APPROACH: FOCUSING ON TOP SUSTAINABILITY RISKS AND OPPORTUNITIES

Since 2014, materiality assessments have been conducted annually and facilitated by a third party to determine the key economic, environmental, social and governance (EESG) issues that are important to our stakeholders. These issues are foundational to CDL’s sustainability strategy, focus and mid-term target setting in our annual sustainability reporting. Corresponding EESG targets, metrics, initiatives, and progress are reviewed by the management team, reported to the BSC and the Board, before they are published annually in our ISR.

In 2025, in alignment with the IFRS S1 and S2, we continued our double materiality assessment looking at both impact and financial materiality, including climate-related risks and opportunities (CROs) affecting the organisation’s financials. CDL’s stakeholders, including the Company’s ExCo, senior management and staff ranked 16 prioritised ESG issues based on both impact and financial materiality. Online surveys were circulated to key stakeholder groups, including the BSC. More than 425 responses were received. Interviews with selected management staff of CDL headquarters and key subsidiaries provided insights into how CDL can manage and strategically address our EESG issues. The preliminary material issues were validated by the Company’s ExCo, senior management and key executives from business units and were reviewed by the BSC thereafter.

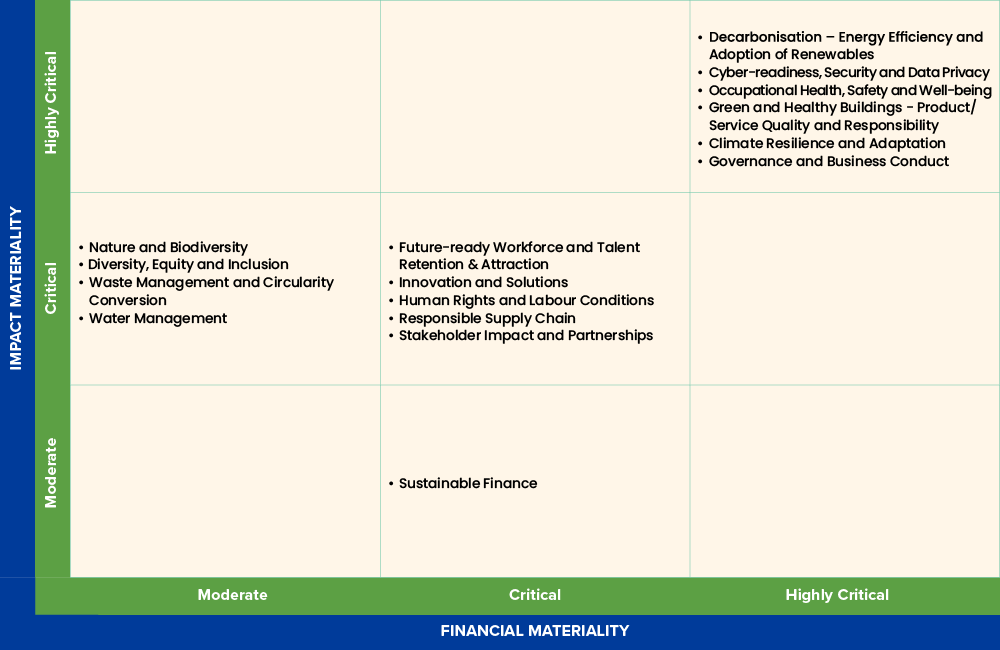

2025 MATERIAL ESG ISSUES

With the urgency of the global energy transition, “Decarbonisation – Energy Efficiency and Adoption of Renewables” remained the top materiality issue in 2025. “Cyber-readiness, Security and Data Privacy” continues to be the 2nd materiality issue, with growing cyber risks of misinformation and disinformation threatening supply chains and financial stability.1 “Green and Healthy Buildings – Product/Service Quality and Responsibility” rose to take 3rd place. All material topics have been categorised either as “Moderate”, “Critical” or “Highly Critical”, signaling that CDL views sustainability as a critical subject across our business and operations.2

- Decarbonisation – Energy Efficiency and Adoption of Renewables

- Cyber-readiness, Security and Data Privacy

- Green and Healthy Buildings – Product/Service Quality and Responsibility ▲

- Occupational Health, Safety and Well-being

- Governance and Business Conduct

- Climate Resilience and Adaptation

- Future-ready Workforce and Talent Retention & Attraction

- Innovation and Solutions

- Human Rights and Labour Conditions ▲

- Stakeholder Impact and Partnerships ▲

- Responsible Supply Chain ▲

- Water Management

- Sustainable Finance ▲

- Waste Management and Circularity

- Nature and Biodiversity Conservation

- Diversity, Equity and Inclusion

Note: ▲ Ranking increased significantly from the previous year’s materiality study.

IDENTIFICATION AND ASSESSMENT OF SUSTAINABILITY-RELATED RISKS AND OPPORTUNITIES (SROs)

In an era of environmental, political, social and economic challenges and despite the recent backlash against ESG, the business case for sustainability remains clear and enduring. Businesses will not thrive on an unhealthy planet gripped by severe climate- and nature-related risks, and capturing opportunities is key to catalyse action towards achieving global climate goals.

Taking reference from ISSB, GRI, TCFD, SASB and CDSB frameworks, an independent consultant was engaged to conduct a study across the Group’s value chain to identify sustainability-related risks and opportunities, mapping to the material issues identified from our latest materiality assessment.

The study extensively mapped all possible risks and opportunities that could affect the Group’s operations or value chain. External factors such as extreme weather events or carbon pricing policies as well as customer-driven factors such as changing demand patterns were considered over varying time horizons, and the likelihood and magnitude of impact were then quantified on a scale of 1 to 5. Given the complex dependencies and relationships, it was important to consider all the pathways and stakeholders which a risk or opportunity could impact. All relevant stakeholders were asked to provide feedback on the scores, before they were aggregated to provide an overall score. In total, there were 470 possible discrete impacts which were aggregated into 40 SROs.

As climate change-related risks and opportunities are deemed to warrant significant attention, our top 10 climate-related SROs were extracted and included in this report to focus on mitigation and adaptation. For more information outlining the Group’s actions in addressing risks and opportunities that are related to our top 17 material ESG issues, please refer to page 41 of the CDL ISR 2025.

Please slide left to view more.

| Rank | SRO | Material issue(s) | Value-chain stakeholders impacted | Business activities | Time horizons |

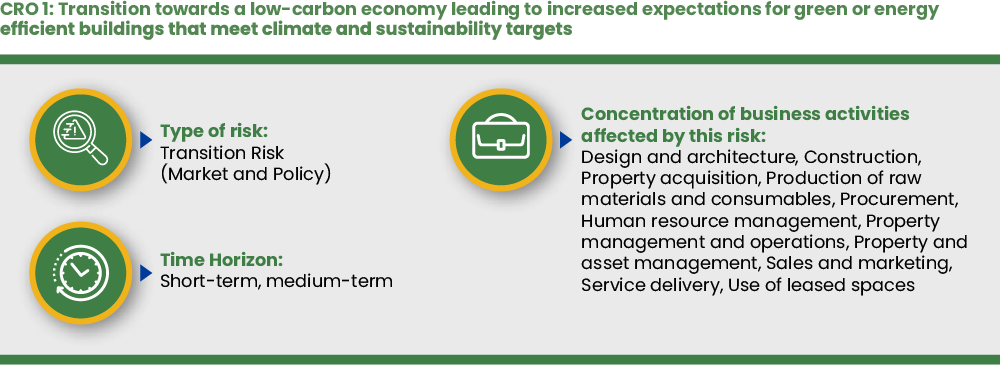

| 1 | Transition towards a low-carbon economy leading to increased expectations for green or energy-efficient buildings that meet sustainability targets for buildings | Energy Efficiency and Adoption of Renewables, Green and Healthy Buildings | All | Design and architecture, Construction, Property acquisition, Production of raw materials and consumables, Procurement, Human resource management, Property management and operations, Property and asset management, Sales and marketing, Service delivery, Use of leased spaces | Short-term, medium-term |

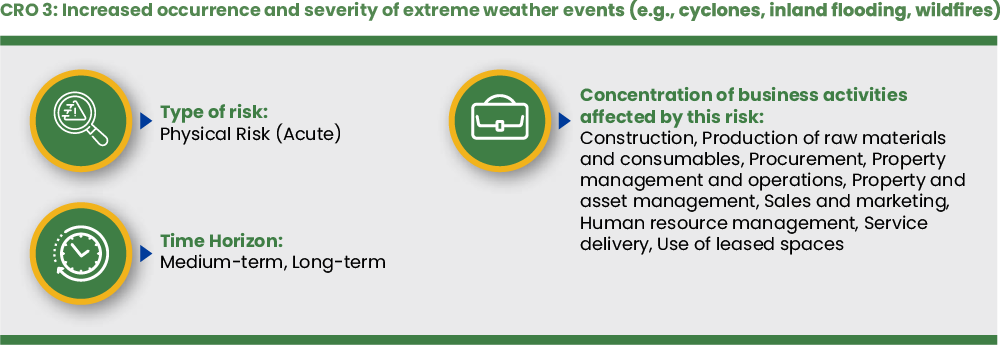

| 2 | Increased occurrence and severity of extreme weather events (e.g., cyclones, inland flooding, wildfires) | Climate Resilience and Adaptation, Governance and Business Conduct, Occupational Health, Safety and Well-being | All | Construction, Production of raw materials and consumables, Procurement, Property management and operations, Property and asset management, Sales and marketing, Human resource management, Service delivery, Use of leased spaces | Medium-term, long-term |

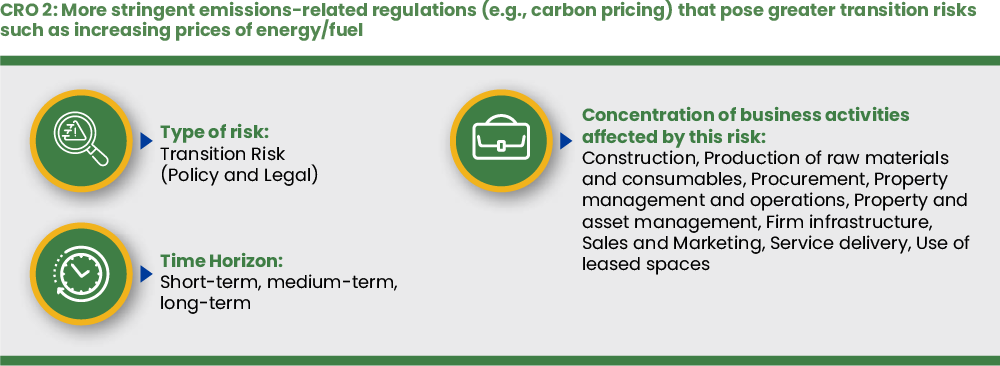

| 3 | Increasingly stringent emissions-related regulations (e.g., carbon pricing) that present transition risks such as increasing prices of energy/fuel | Energy Efficiency and Adoption of Renewables, Responsible Supply Chain, Climate Resilience and Adaptation | All | Construction, Production of raw materials and consumables, Procurement, Property management and operations, Property and asset management, Firm infrastructure, Sales and marketing, Service delivery, Use of leased spaces | Short-term, medium-term, long-term |

| 4 | Increasing expectations to incorporate ESG factors in investment management and supply chain management | Climate Resilience and Adaptation, Energy Efficiency and Adoption of Renewables, Sustainable Finance | Upstream, Own operations | Construction, Production of raw materials and consumables, Procurement, Human resource management, Property management and operations, Property and asset management, Sales and marketing, Service delivery | Short-term, medium-term, long-term |

| 5 | Increasing demand and supply for sustainable products and low carbon solutions for climate adaptation and mitigation (e.g., green buildings, green leases, green bonds) | Energy Efficiency and Adoption of Renewables, Green and Healthy Buildings, Innovation, Product/Service Quality and Responsibility, Sustainable Finance | Upstream, Own operations | Design and architecture, Construction, Technology Development, Production of raw materials and consumables, Property acquisition, Procurement, Human resource management, Financing and investment, Property management and operations, Property and asset management, Sales and marketing, Service delivery | Medium-term, long-term |

| 6 | Increasing options for greener energy sources (e.g., renewable energy, alternative fuel, etc.) | Energy Efficiency and Adoption of Renewables | Upstream, Own operations | Production of raw materials and consumables, Procurement, Human resource management, Property management and operations, Property and asset management, Sales and marketing, Service delivery | Medium-term |

| 7 | Increasing nature-based solutions to reduce emissions and environmental impact | Nature and Biodiversity Conservation | Upstream, Own operations | Construction, Technology Development, Human Resource Management, Sales and marketing, Service Delivery | Medium-term |

| 8 | Incentives provided by government entities for climate adaptation and mitigation solutions | Sustainable Finance | All | Financing and investment, Property management and operations, Property and asset management, Technology development, Use of leased spaces | Medium-term |

| 9 | Implementation of climate risk mitigation strategies on water and wastewater infrastructure (e.g., diversification of water supplies, sustainable withdrawal levels, etc.) | Water Management | Upstream, Own operations | Construction, Property management and operations, Property and asset management, Sales and marketing, Service delivery | Medium-term |

| 10 | Increased cost of materials and consumables due to supply chain vulnerabilities | Responsible Supply Chain | Upstream, Own operations | Production of raw materials and consumables, Procurement, Construction, Property management and operations, Property and asset management | Short-term |

| 1 | World Economic Forum, Global Risks Report 2025. |

| 2 | There are no major changes to the material topics, except for the renaming of two material topics (“Decarbonisation – Energy Efficiency and Adoption of Renewables” and “Innovations and Solutions”) and the merging of “Product/ Service Quality and Responsibility” into “Green and Healthy Buildings – Product/ Service Quality and Responsibility”. |

IDENTIFICATION AND ASSESSMENT OF SUSTAINABILITY-RELATED RISKS AND OPPORTUNITIES – QUANTIFICATION OF TOP THREE CROS

Taking reference from the ISSB, GRI, TCFD, SASB and CDSB frameworks, an independent consultant was engaged to conduct a study in 2024, involving internal and external key stakeholders across the Group’s value-chain, to identify sustainability-related risks and opportunities (SROs).

Among the SROs identified, climate-related risks and opportunities (CROs) were deemed the most significant. The top three CROs were extracted and quantified in this report to enable focused mitigation and adaptation. For more information outlining the Group’s actions in addressing risks and opportunities that are related to our top 16 material ESG issues, please refer to pages 28-37 of the CDL ISR 2026.

Description of Risk

With increasing expectations for SLE buildings, CDL is expected to decarbonise existing and new assets to meet increasingly stringent sustainability standards.

Different jurisdictions worldwide have established varying carbon prices. In addition to other climate-related regulations, this may increase operating costs. In our key market in Singapore, to support its net-zero target, carbon tax will be raised from S$25/tCO2e in 2024 to S$45/tCO2e in 2026 and 2027, with a view to reaching S$50-80/tCO2e by 2030. This creates a direct financial penalty for carbon-intensive operations. Under the Singapore Green Building Masterplan, “80-80-80 in 2030”, properties that do not meet high energy-efficiency standards (e.g., BCA Green Mark Platinum or SLE) risk becoming “brown assets”. Brown assets could face lower demand, reduced capital value, and higher insurance premiums. Overall, higher operational costs from decarbonisation initiatives may affect the competitiveness of our assets, especially when compared to competitors operating in jurisdictions with less regulatory requirements. Potential loss of green rental premium is also a risk, if we do not provide sustainable spaces that meet tenant and customer demands.

As the Singapore market has the largest proportion of Development Properties (DPs) and Investment Properties (IPs) amongst the six markets studied in our 4th Climate Change Scenario Analysis, these are the two property types that will be affected by increased cost of materials, green construction cost premium, and potential loss of green rental premium revenue, which contribute to CRO 1.

Mitigation Efforts

- To mitigate these risks, CDL has set ambitious net-zero carbon operational targets for our buildings to align with a low-carbon future and stakeholder expectations. These goals are aligned with global net-zero goals and follow frameworks such as the Glasgow Financial Alliance for Net Zero (GFANZ) and the Transition Plan Taskforce (TPT). CDL also targets for 80% of our owned and managed assets to achieve BCA Green Mark SLE status by 2030 and has set a target to reduce embodied carbon intensity by 41% by 2030.

- To support the achievement of these goals, CDL’s Climate Transition Plan integrates climate action into its business model and value creation strategy. We have also developed the CDL Sustainable Investment Principles to steward responsible capital allocation and decision-making for investments.

- CDL has been continually investing in green design and features for its new developments. The requirement of green building classifications is expected to get more stringent over time in both the 1.5 degree scenario (DS) and >3DS, and as such, there is an expected increase in cost to design and construct buildings that follow such standards. For more information on this, please refer to Chapter 3 of the CDL ISR 2026.

Adaptation Efforts

CDL has a range of adaptation efforts designed to manage the risks posed by increasing demand for green buildings, alongside its mitigation strategies. We design new developments and existing assets towards having high-performance, energy-efficient, and low-carbon outcomes. These include the following:

- Green building certification: As of December 2025, we achieved 130 BCA Green Mark certifications, reinforcing competitiveness and compliance.

- Asset retrofits: Older assets are retrofitted to improve energy performance, maintain competitiveness, and ensure long‑term sustainability through proactive life‑cycle planning.

- Internal carbon pricing (ICP): CDL carried out an ICP pilot to study carbon prices for investment decisions to account for environmental costs.

- Climate scenario analyses: Since 2018, CDL has conducted four climate scenario studies to better understand the financial impact from climaterelated risks. In December 2025, we concluded our fourth study, expanding to six key markets, with time horizons extended beyond 2030 to include 2040 and 2050, and more granular analysis carried out at the asset level. For more information, please refer to Chapter 3 of the CDL ISR 2026.

- Climate-proofing governance: Climate-related risks and transition scenarios are integrated into enterprise risk management and strategic planning to ensure future-ready, resilient assets.

- Green lease and tenant engagement: Since 2017, the Company has achieved 100% retail and office tenant participation in the CDL Green Lease Partnership Programme. The Company first piloted the City Green Tenant Bonus (CGTB) Programme in 2024. In 2025, we recognised tenants who achieved at least a 10% reduction in their energy use.

Current Financial Effects

Green construction premium: Based on CDL’s ongoing projects under construction in Singapore, the Group estimates that the green cost premium incurred (cash outflows) in developing buildings that meet the planned Green Mark certification is between S$4.7 million to S$24.1 million. This excludes overseas projects under constructions such as China, UK and Australia, due to lack of available data at present to reliably estimate the green construction premium for these foreign jurisdictions.

Anticipated Financial Effects

Green construction premium: The Group anticipates to incur a green construction premium of up to S$70 million over the time horizon of 2026 to 2030. This reflects the incremental costs required to develop buildings that meet the planned Green Mark Certifications, consistent with the Group’s transition strategy and decarbonisation pathway. The estimate has been derived based on existing projects under development in Singapore and is based on current market assumptions regarding green construction specifications and costs benchmarks. The estimate excludes overseas projects currently under construction and any potential future developments due to limited data availability and measurement uncertainty regarding cost comparability across jurisdictions. At this stage, the Group is unable to estimate the anticipated financial effect for the medium to long-term horizon (beyond 2030) due to uncertainty in the future cost trajectory of low-carbon and green construction materials, variability in the number, scale, and location of the projects the Group may undertake in the future, and the evolving nature of certification standards and regulatory requirements.

The Group will continue to update these estimates as methodologies, data availability, and market inputs evolve, and as additional information becomes available on future development pipelines and green construction cost benchmarks.

Cost savings: The Group estimates that the cost savings achieved from the abovementioned Singapore green buildings to be S$22.9 million over the life cycle of these buildings.

Description of Risk

For CDL, the transition to a low-carbon economy presents a significant financial and operational challenge. As governments in our key markets ramp up carbon pricing and emissions regulations, CDL faces a dual-pronged risk: rising direct costs and a potential devaluation of carbon-intensive assets. Similar to CRO 1, properties that fail to meet tightening energy standards risk becoming stranded assets and may face accelerated depreciation and lower market value. An increase in carbon taxes and fuel prices across jurisdictions and CDL’s key markets will also affect our bottom line through direct operational and compliance costs. For example, in Singapore, our highest impact market, carbon tax is projected to rise to S$50-80/ tCO2e by 2030. The Group’s value chain and supply chain is also impacted by this risk. As carbon pricing hits steel and cement manufacturers, we face a green construction cost premium, with the price of low-carbon materials being higher than conventional ones.

Mitigation Efforts

Some of the mitigation efforts to manage increasingly stringent emissions-related regulations include:

- Asset retrofits: Older assets are retrofitted to improve energy performance (e.g., chiller plants, energy efficient lighting).

- Renewable assets: CDL adopts renewable energy by tapping on solar power through rooftop photovoltaic panels in commercial assets.

- CDL has transitioned from diesel generators to Energy Storage Systems at construction sites (e.g., Irwell Hill Residences) to reduce fuel reliance when feasible.

- Internal carbon pricing (ICP) pilot: In 2024, CDL completed an ICP pilot at Republic Plaza, our flagship commercial asset, to assess mitigation costs and inform a carbon price pathway towards net-zero. CDL continues to refine the use of ICP to raise awareness of carbon costs and deepen the integration of environmental considerations into financial decision-making.

Adaptation Efforts

- CDL’s WorldGBC Net Zero Carbon Buildings Commitment: By pledging to achieve net-zero operational carbon by 2030 under the WorldGBC Net Zero Carbon Buildings Commitment in February 2021, we have set goals and aligned our decarbonisation roadmap strategies accordingly. This has helped us to mitigate future compliance risk with stricter emissions regulations and carbon pricing regimes.

- Green lease and tenant engagement: CDL’s tenant engagement and green lease programmes encourages and incentivises tenants to reduce energy consumption and adopt sustainable office practices. In the long term, behavioural change contributes to lower energy consumption and operational costs.

Current and Anticipated Financial Effects

Since 2012, cumulative capital expenditure on energy-efficient retrofits undertaken for locally managed investment properties amounts to approximately S$54 million. These initiatives include high-efficiency chillers, building management system optimisation, LED retrofits and other energy-performance enhancements. The related equipment costs are recognised within the cost of investment properties and depreciated over their useful lives.

These retrofits contributed to approximately S$3.5 million/year in electricity cost savings and reductions to cash outflows for FY2025. These savings are reflected within operating expenses and cost of sales in the statement of comprehensive income and contribute positively to the Group’s profit before tax. From 2012 to 2025, the cumulative energy cost savings is approximately S$47.5 million.

Based on a carbon tax rate of S$45 per tonne, the Group anticipates the annual savings in electricity cost of approximately S$3.5 million/year to continue from 2026 to 2030. This estimate is subject to underlying assumptions relating to electricity tariffs, carbon pricing and asset performance. Under higher electricity price or carbon tax scenarios, the expected savings would increase proportionally.

The above current and anticipated financial impacts relate to the Group’s managed investment properties in Singapore and excludes overseas investment properties and hotel properties. The Group is in the process of gathering the required information to quantify the climate-related financial effects of energy-saving initiatives undertaken by hotels and overseas properties. These amounts are not currently available without undue cost or effort.

Description of Risk

Extreme weather causes significant property damage and business disruption globally today. Increases in severity of these hazards are likely to increase business damage and disruption such as property damage, delay in construction, compensation to tenants, increase in insurance premiums, and indirect loss in hotel revenue from property damage and long-lasting damage to the cultural value of eco-tourism areas.

In our 4th Climate Change Scenario Analysis, six key markets studied – Singapore, US, China, Japan, New Zealand and the UK – are exposed to extreme weather events, albeit of different type and nature. Tropical cyclones was one of the top three physical risks identified. Based on the findings of the third (2019 baseline) study, the Group’s US market had the biggest total physical risk exposure to extreme events. However, due to the introduction of coastal flooding as a risk, Singapore has the largest exposure to extreme events in the current study, with the US following closely. In both the 3rd and 4th study, the UK market experienced the highest risk from floods (flash and river, with the inclusion of coastal this year).

Mitigation Efforts

CDL is committed to reducing the carbon footprint of our assets to limit the long-term severity of global climate change.

- In February 2021, CDL pledged its commitment to the WorldGBC Net Zero Carbon Buildings Commitment and aims to have all wholly-owned assets to be net zero by 2030.

- Develop plans to increase decarbonisation capabilities of our suppliers: Increased focus on management of Scope 3 emissions: Launched the first SME Supplier Decarbonisation Queen Bee Programme in 2024 to help SME suppliers strengthen decarbonisation efforts. This supports and incentivises CDL’s value chain and ecosystem of stakeholders to learn how to effectively decarbonise.

Adaptation Efforts

- The Company is the first public-listed company in Singapore to adopt TNFD recommendations to use nature-based solutions (e.g., rain harvesting, vertical walls etc.) to also complement climate mitigation and adaptation strategies.

- As far as practicable, CDL adopts the following principles for its new developments:

- Apply EHS risk assessments at concept, design, and construction stages, which include assessment of flooding risks for projects located at low lying areas.

- Incorporate Active, Beautiful, Clean Waters (ABC) Waters Design Guidelines in environmentally sustainable features including measures to (1) retain and control stormwater runoff to minimize flooding risk and (2) treat stormwater runoff to reduce impurities discharged into water systems.

- Incorporate sustainable landscape design features like roof and rain gardens to help retain and control stormwater runoff. 70% of Irwell Hill Residences’ ground area comprises lush landscape and facilities, with a sky and roof garden.

- Crest levels for entrances to underground structures are designed to be at least 150 mm to 300 mm above the building ground level to prevent flooding to the basement.

- Flood protection measures such as automated or manual flood barriers and water-level sensors are also required. To reduce direct heat, buildings are oriented to be north-south facing.

Current and Anticipated Financial Effects

In 2025, no climate-related extreme event has occurred affecting the Group’s properties or operations. Therefore, there has been no impairment loss recognised or repair and replacement cost incurred by the Group in 2025 as a result of extreme weather events.

During the year, the Group did not require additional mitigation measures targeted at extreme climate events. Climate adaptation considerations have been incorporated into the design, planning and construction of all new development projects to enhance the long-term resilience to climate-related risks. The associated costs of these adaptation features are integrated within broader development budgets and cannot be separately determined or reliably quantified at this stage.

For existing completed properties, the Group expects that capital expenditure on climate mitigation measures will increase over time, driven by the physical risks anticipated to affect the Group’s properties. These investments are intended to enhance asset resilience and reduce potential operational and financial impacts arising from climate‑related physical risks.

The increased risks associated with extreme weather events may lead to higher property insurance premiums. At present, insurance costs related specifically to climate‑related risks are not separately identifiable from the Group’s overall insurance premiums. As such, the Group is unable to reliably estimate the near‑term financial impact of potential increases in insurance premiums. Nevertheless, based on the results of the Group’s fourth climate change scenario study, the Group anticipates an additional insurance premium cost of approximately S$8 million by year 2050 under the 3°C warmer scenario. This estimate is subject to significant estimation uncertainty due to the long‑term nature of the assumptions, evolving climate risk exposures, and potential changes in insurance market conditions.