4th CLIMATE CHANGE SCENARIO ANALYSIS

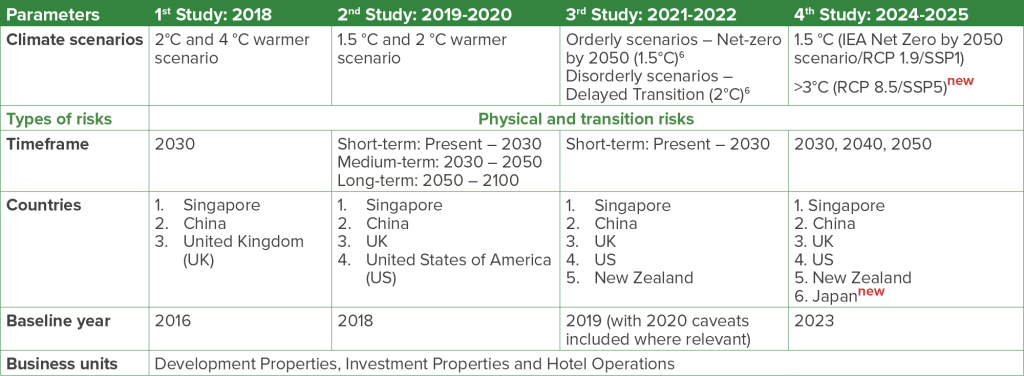

Since we adopted the Task Force on Climate-Related Financial Disclosures (TCFD) Recommendations in 2017, CDL has conducted a total of four climate change scenario analyses. The climate change scenario analysis, which is now a recommendation of the International Financial Reporting Standards (IFRS) S2, aids corporates in understanding the strategic implications of climate-related risks and opportunities.

Climate Change Scenario Study: Risks Identification, Categorisation And Mitigation

Facilitated by an independent consultant, the Company completed our 4th climate change scenario study in December 2025 to better understand the short-, medium- and long-term financial implications of climate change on our business. The study identified, categorised and prioritised climate-related physical and transition risks based on the expected financial impact of the risk and opportunities it addresses.

In this 4th study, the following key changes were applied:

- The Group has included Japan as a sixth market, along with additional property coverage in other locations

- Compared to the 3rd study, analytical parameters have been enhanced, with temperature pathways now including a scenario exceeding 3°C, alongside lower emission pathways

- Time horizons have been extended beyond 2030 to include 2040 and 2050, aligning with IFRS S2 expectations for resilience assessments using multiple plausible climate scenarios over short, medium, and long-term horizons

- Analysis was done on an asset level, allowing for much more granular data to be used. Recommendations from emerging climate-related developments such as COP29, Intergovernmental Panel on Climate Change Sixth Assessment Report (IPCC AR6), and the Taskforce on Nature-related Financial Disclosures (TNFD) were also used

Risk Management and Strategic Decision-making Process

At the Group level, we adopt an integrated top-down and bottom-up risk review process that enables systematic identification and prioritisation of all material transition and physical risks. The Board, supported by the Audit & Risk Committee (ARC) and other Board committees, assumes responsibility and oversight of the key risks to the Group’s business. Relevant and material risk issues are surfaced for information and discussion with the ARC and the Board minimally every quarter. The ARC considers the nature and extent of significant risks which the Group may undertake in achieving our strategic objectives, and guides management in the formulation and implementation of the risk management framework, policies, and processes. This ensures that significant risks are effectively identified, evaluated and mitigated, to safeguard shareholders’ interests and the Group’s assets.

The ARC also reports to the Board on critical risk issues, material matters, findings, and recommendations. Risk mitigation measures were identified and integrated into operations through the Company’s Enterprise Risk Management (ERM) framework. We manage risks by tracking interim performance against our CDL FV2030 targets, refining our environmental management systems and carbon performance metrics, in line with global standards such as the GHG Protocol and ISO 14064.

Scope And Parameters Of The Four Studies

Key Findings From 4th Climate Change Scenario Analysis

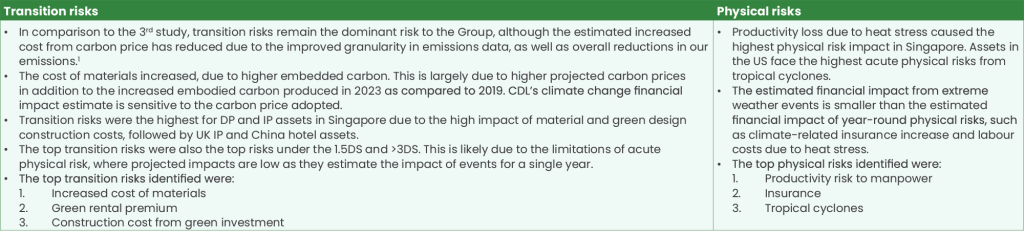

- Out of the six markets studied, Singapore has the largest proportion of Development Properties (DPs) and Investment Properties (IPs). These are the two property types that are most affected by the top three most transition risks – increased cost of materials, green construction cost premium, and potential loss of green rental premium revenue

- As a result, for both the 1.5 degree scenario (DS) and >3DS, Singapore is the country with the highest estimated annual incremental financial impact from both climate-related risks and opportunities. China faces the next highest impact, while New Zealand faces the least impact

| 1 | There were a large number of changes between the third (2019 baseline) study and fourth (2023 baseline) study, largely attributed to changes in CDL’s business operations, granularity of information, as well as revisions in methodology to accommodate the additional timeframes. Therefore, the comparison between the total annual incremental financial impact in year 2030 from the third study and the fourth study is not a direct one-to-one comparison. |